As I wrote in an article published in French in the Luxembourger Wort Thursday May 20, the construction of Europe, and even more so the euro-zone, has for many years become dogmatic and not pragmatic: momentum became the sake of the EU objective, and short-term fixes the rule of law as evidence with the Maastricht Treaty criteria and the Stability Pact which have repeatedly been trampled underfoot. European politicians disregarded macroeconomic imbalances within the euro-zone and budget profligacy that led to the worse crisis since its creation which threatens the survival of the euro itself.

1. Euro-zone macroeconomic imbalances

Structural macroeconomic imbalances within the euro-zone widened and the financial crisis triggered earlier what was inevitable: a sovereign debt crisis in Europe that will dwarf the sub-prime rout if not properly addressed very quickly.

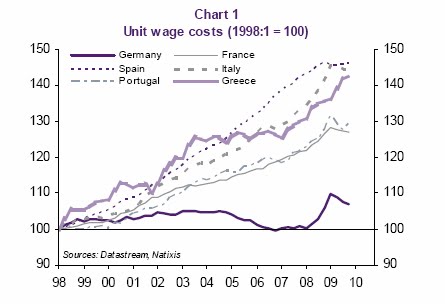

Among these macroeconomic imbalances, competitiveness is probably the one that illustrates best the current crisis with the deterioration of the southern euro-zone countries compared with countries in the north.

Growth in these countries was also mainly supported by consumption with led to recurring trade deficits.

Growth in these countries was also mainly supported by consumption with led to recurring trade deficits.

1. Euro-zone macroeconomic imbalances

Structural macroeconomic imbalances within the euro-zone widened and the financial crisis triggered earlier what was inevitable: a sovereign debt crisis in Europe that will dwarf the sub-prime rout if not properly addressed very quickly.

Among these macroeconomic imbalances, competitiveness is probably the one that illustrates best the current crisis with the deterioration of the southern euro-zone countries compared with countries in the north.

2. Unsustainable budget deficits and public debt in Europe

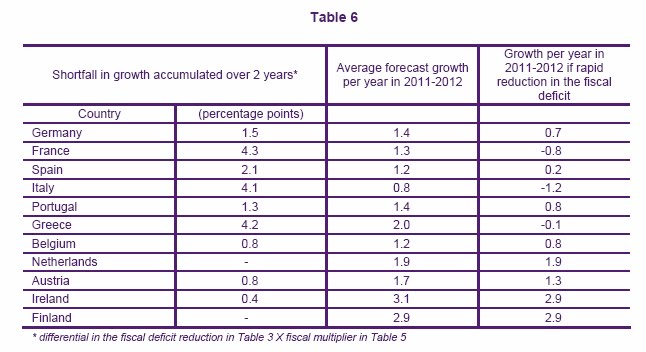

In this blog, I have already provided many information regarding the debt/GDP and budget deficit/GDP, showing deteriorating trend and unsustainability. Austerity measures have been announced in most countries with large budget deficits and debts. I doubt it will be possible to implement many of them being too late, too much for such a short period of time.

If implemented, according to Natixis, the French bank, this would result in a cumulative growth shortfall of over 4% for France, Greece and Italy in 2011-2012.

They conclude:

This shows that:

− either the reduction in fiscal deficits will be slower, with the risk of a negative reaction by the financial markets;

− or other measures to stimulate the economy will be implemented, for instance policies aimed at depreciating the euro (quantitative easing).

Whatever, the euro will head south until the eurozone put its acts together and move from dogmatism to pragmatism.

Let's now have a look at the problem under a different angle than the usual debt/GDP or deficit/GDP. Does it make sense indeed, to compare the GDP - the wealth a nation creates every year - with a budget deficit or a public debt that result from State budget imbalances, and the lack of tax revenues or excess expenses? I don't think so, even if it is an easy fix which, I must confess, I very often use.

So, what are tax revenues / debt and budget deficits / tax revenues to have a true picture of the efforts needed to overcome these historical and difficult times.

If you add an environment of exceptionally low interest rates, the situation could worsen very quickly. For example, France interest payments on its debt represents 2.5% of GDP; if interest rates were to increase by a mere 1% it would imply EUR 10 billion of additional payment; if interest rates were to increase from 3% to 7%, it would amount to EUR 100 billion, or 5.2% of GDP and 28% of the budget! This exemplify the precarious situation of not only the PIGS countries but also France, Italy and the UK (outside the euro-zone).

It also explains the skepticism of markets and the fall of the euro.

I do not see how, at least Greece will escape a restructuring of its debt. After all Dubaï World did it as detailed in an interesting Bloomberg article:

"Dubai World, the state-owned holding company, agreed “in principle” with a group of creditor banks on terms to restructure $14.4 billion of loans.

Dubai World will pay $4.4 billion in five years and the remaining $10 billion in eight years, the company said in an e- mailed statement today. Banks will have the option to choose from combinations of loan maturities in dollar or dirhams that carry different interest rates. Including the Dubai government’s debt the total liabilities being restructured is $23.5 billion.

Banks will be paid 1 percent interest on $4.4 billion of the loans maturing in five years. The lenders have three options in the eight-year maturities covering about $10 billion of debt with at least 1 percent interest and varying additional rates between 1.5 percent and 2.5 percent at maturity. Two of these options also have a shortfall guarantee."

Source:

Bloomberg: Dubai World, Creditors Reach $23.5 Billion Debt Deal

http://www.bloomberg.com/apps/news?pid=20601087&sid=ausEikB1RsxY&pos=2

Natixis: Flash economics -The dangers of the "conservatism" of certain analyses of the euro zone’s problems

http://cib.natixis.comflushdoc.aspx?id=53163

http://cib.natixis.com/flushdoc.aspx?id=53156