As readers of Markets & Beyond know, I am closely following the implementation of the Greek budget. Its most recent release (20 October) leads me to conclude that the Economic Policy Program (“EPP”), which takes into account stability measures decided in March and May and implemented since, will not be met.

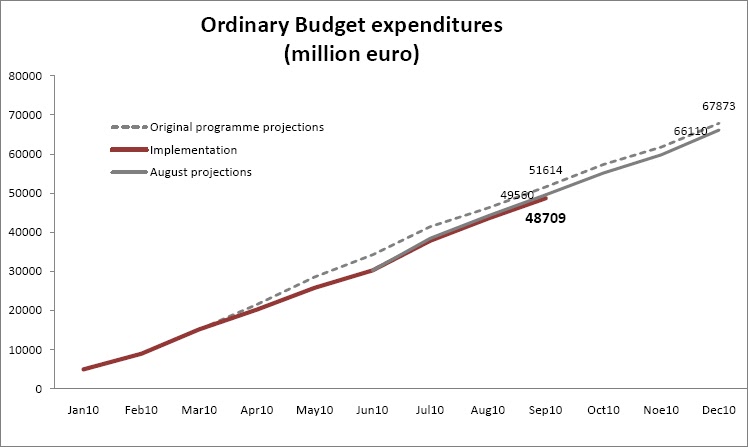

At the end of September, cumulated revenues were running behind schedule at EUR 36.5 billion whilst they should be standing at EUR 41.4 billion (EUR 55.1 billion projected for 2010); the gap between projection and realization is widening: the latest data from the Greek Ministry of Finance indicate that EUR 2.4 billion revenues will not materialize with direct tax and indirect tax 10% behind schedule so far. The growing gap between tax revenues and EPP leads me to also doubt about the GDP growth forecast.

Overall the improvement compared to the disastrous 2009 is obvious but trailing projections despite the harsh measure taken by the Greek Government and money poured y the ECB (for banks), the EU and the IMF (to match the borrowing requirements). This leaves us with a budget deficit which should be close to EUR 21-22 billion (pending numbers massaging by the EU and the Greeks). As stated in previous articles, Greece has the problem with revenues more than costs; yes, they must slim down but due to the sheer size of its debt, it is a substantial increase in revenues that will save Greece from default/restructuring, and frankly I do not see how they can avoid it.

Finally, on 20th October Eurostat released an update for EU 2009 budgets deficits for all member states but Greece:

“Eurostat has completed its enquiries on statistical compilation of the Greek fiscal data and is now undertaking a process of quality assessment of statistical source data from public accounts, in cooperation with the Greek Statistical Office and the Greek Court of Auditors. Following this process, and the release of the annual report of the Greek Court of Auditors at the beginning of November 2010, Greek fiscal data will be published by Eurostat by mid November 2010.”

On October 27, the Finance Minister, George Papaconstantinou, said a review of the 2009 budget showed the deficit was greater than 15 percent of gross domestic product, more than the 13.6% previously estimated, and more than what he said on October 7…

The final number will be published by Eurostat by mid November.

As for banks, it is time to stop bailing out cheaters and incompetents: imagine to what productive use and wealth creation the trillions of wasted money could have bee channeled to.

Source:

Greek Ministry of Finance: Budget Execution 2010 – September

http://www.minfin.gr/content-api/f/binaryChannel/minfin/datastore/13/22/51/1322514373507c0e5ac9891e0341704781f4c40d/application/pdf/Budget+Execution+Bulletin-+September+2010.pdf

Greek Ministry of Finance: Presentation on Budget Execution / January-September 2010

http://www.minfin.gr/content-api/f/binaryChannel/minfin/datastore/47/2d/e2/472de2e55ba77ae92d7972c7079c1cef806a66d0/application/pdf/Presentation+on+Budget+Execution.pdf

Eurostat: Euroindicators - Second notification of government deficit and debt figures for 2009

http://epp.eurostat.ec.europa.eu/cache/ITY_PUBLIC/2-22102010-AP/EN/2-22102010-AP-EN.PDF

Bloomberg: Greek Bonds Tumble as Government Says Tax Revenue Falling Short

http://www.bloomberg.com/news/2010-10-27/greek-bonds-drop-as-tax-collection-falls-short-of-government-revenue-goal.html

{kind=link}