When the EBA stress tests on 90 European banks were

published in July, I titled them a mockery. I conducted my own analysis according to a 50% and 75% haircut on sovereign

debt in PIIGS countries to abide by the 9.5% core capital to be reached by 2019

according to Basle III rules (many banks said they would get there well ahead

of time): this analysis produced the numbers I mentioned in several articles on

this blog.

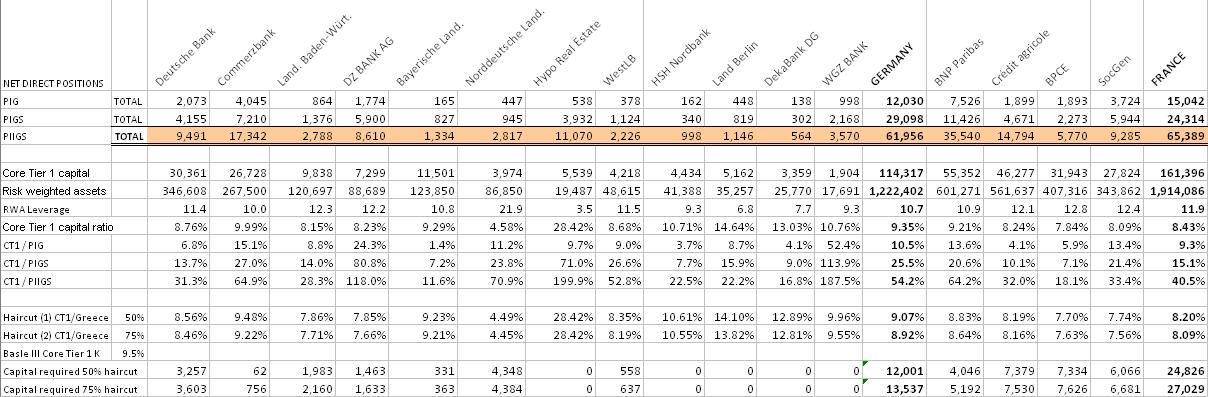

In the table below, let’s look at German and French banks’

exposure to the Greek sovereign debt (being the main holders, I do not include

other banks):

A 50-75% Greek

default would result EUR 36 and 40 billion new capital required, split 1/3 for

Germany and 2/3 for France. This does neither take into account their

exposure to the banking and private sector nor guarantees/commitments/derivatives

(including CDS). The German situation is not much worse with respectively EUR

9.7 billion additional exposure (including EUR 2.1 billion with Greek banks)

and EUR 5.3 billion; French banks’ are in a much more difficult position with EUR

43.5 billion (including EUR 1.6 billion for banks) and EUR 8.3 billion.

To be fair, these numbers reflect the situation at the end of December 2010 and French banks have significantly reduced their exposure on their Greek sovereign debt during H1 2011: BNP Paribas from EUR 5 billion to EUR 3.5 billion and Société Générale from EUR 2.7 to EUR 1.9 whilst producing a net 6 months result of EUR 4.7 billion and EUR 1.6 billion, so enough to absorb a 100% default. However, as for Dexia that went under mainly because of its exposure to the non-sovereign credit book, I do not know what the quality of the private book is.

To be fair, these numbers reflect the situation at the end of December 2010 and French banks have significantly reduced their exposure on their Greek sovereign debt during H1 2011: BNP Paribas from EUR 5 billion to EUR 3.5 billion and Société Générale from EUR 2.7 to EUR 1.9 whilst producing a net 6 months result of EUR 4.7 billion and EUR 1.6 billion, so enough to absorb a 100% default. However, as for Dexia that went under mainly because of its exposure to the non-sovereign credit book, I do not know what the quality of the private book is.

Let’s add a 100% default on Greek banks and 15 % on the

private sector (guarantees and commitments included but not derivatives), the banking needs required to abide by

Basle III rules is north of EUR 50 billion for German and French banks that

were subject to the EBA stress test.

The total number of

EUR 100 billion rumored to be in the starting blocks to recapitalize European

banks is probably right on a Greek basis alone. In order to weigh the

minimum possible on government budgets already under dramatic strain, this

recapitalization should be undertaken via profits, cutting dividends to zero and

reducing bonus payments (say by the same amount as the Greek default). It is however far from addressing the rest

of BIGSPIF sovereign risk.

Nevertheless, the EUR 100 capitalization does not address

the core of the matter: the sovereign insolvency and lack of economic

competitiveness. More on this in a forthcoming article: France - EZ weak link.

BIGSPIF = Belgium, Ireland, Greece, Spain, Portugal, Italy, France